Introduction

Life insurance is one of the most important financial tools available to individuals and families. Yet, many people either misunderstand it or delay purchasing it until it is too late. In this comprehensive guide, we will explain what life insurance is, how it works, the different types available, and why it matters for your financial future.

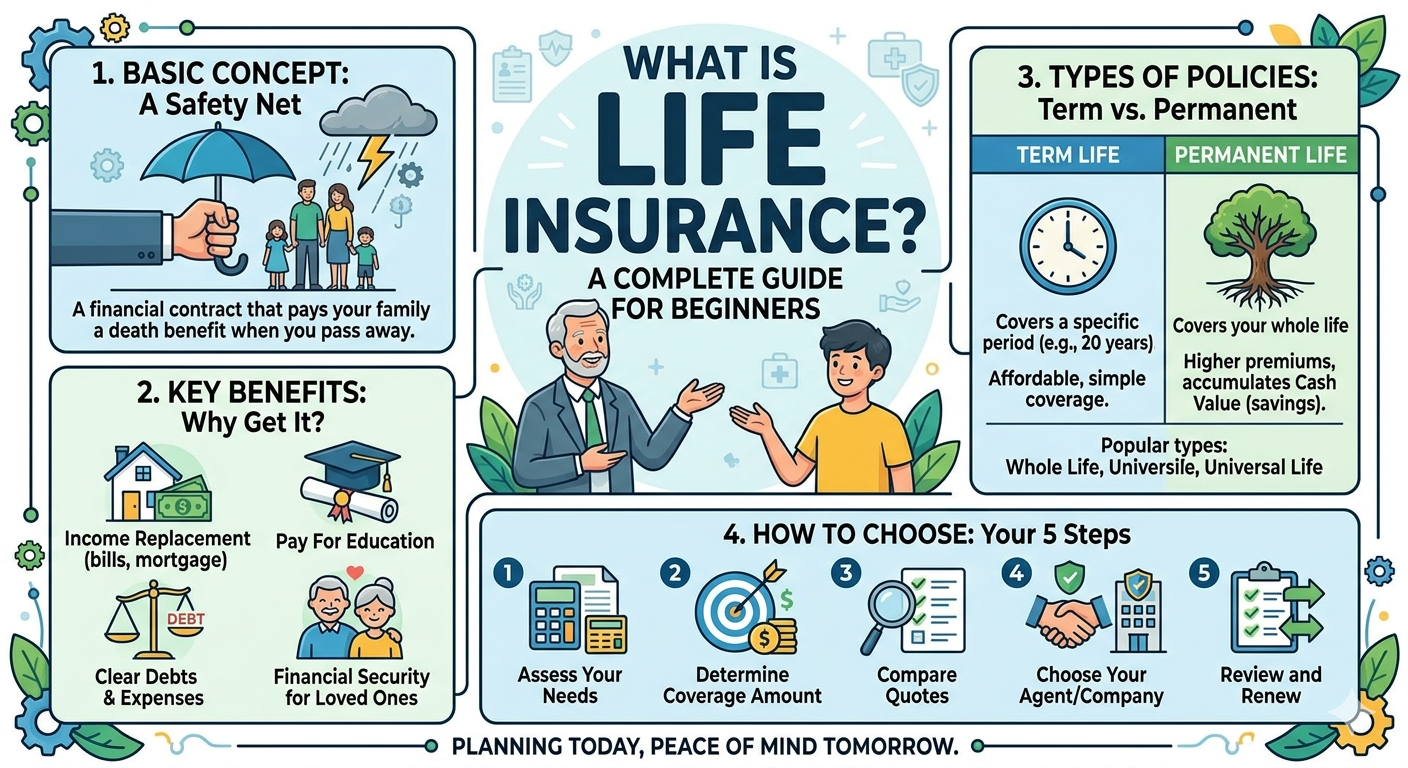

What Is Life Insurance?

Life insurance is a legal contract between you (the policyholder) and an insurance company (the insurer). In exchange for regular premium payments, the insurer promises to pay a designated sum of money — known as the “death benefit” — to your chosen beneficiaries upon your death. This financial protection ensures that your loved ones are not left struggling with financial hardship after you are gone.

Why Is Life Insurance Important?

The primary purpose of life insurance is to provide financial security to your family. Consider these key reasons why life insurance matters:

- Income Replacement: If you are the primary earner in your family, your sudden death could leave your dependents without a stable income. Life insurance replaces that lost income.

- Debt Coverage: Outstanding loans such as mortgages, car loans, or personal debts do not disappear when you die. A life insurance payout can settle these obligations.

- Education Funding: Parents often use life insurance to ensure their children’s education is funded even if they are no longer alive.

- Funeral Expenses: Funeral and burial costs can be significant. Life insurance can cover these expenses so your family does not bear this burden.

- Peace of Mind: Knowing that your family is financially protected gives you genuine peace of mind during your lifetime.

Types of Life Insurance

Understanding the different types of life insurance helps you choose the right policy for your needs.

Term Life Insurance

Term life insurance provides coverage for a specific period — typically 10, 20, or 30 years. If you die within the term, your beneficiaries receive the death benefit. If you outlive the term, the policy simply expires. Term life insurance is the most affordable option and is ideal for young families and individuals with temporary financial obligations.

Whole Life Insurance

Whole life insurance provides permanent coverage for your entire lifetime. In addition to the death benefit, whole life policies accumulate a “cash value” component that grows over time. You can borrow against this cash value or use it as a savings vehicle. Whole life insurance is more expensive than term insurance but offers lifelong protection.

Universal Life Insurance

Universal life insurance is a flexible permanent policy that allows you to adjust your premiums and death benefit over time. It also builds cash value, but the growth is typically tied to current interest rates. This type is suitable for individuals who want flexibility in their coverage.

Variable Life Insurance

Variable life insurance allows you to invest the cash value portion into various investment funds such as stocks or bonds. The death benefit and cash value can fluctuate based on the performance of your investments. This option carries more risk but also offers the potential for higher returns.

How Much Life Insurance Do You Need?

A common rule of thumb is to purchase life insurance coverage equal to 10 to 12 times your annual income. However, the ideal amount depends on several personal factors:

- Your current income and expected future earnings

- The number of dependents who rely on you financially

- Outstanding debts such as mortgages or loans

- Your family’s lifestyle and monthly expenses

- Future goals such as children’s education or retirement

Many financial advisors recommend using the DIME method (Debt, Income, Mortgage, Education) to calculate the right coverage amount.

How to Choose the Right Life Insurance Policy

Selecting the right policy requires careful consideration. Here are some steps to guide you:

Step 1 – Assess Your Needs: Evaluate your financial situation, family size, and long-term goals.

Step 2 – Set a Budget: Determine how much you can afford to pay in premiums each month.

Step 3 – Compare Policies: Use online tools or consult an insurance agent to compare multiple policies.

Step 4 – Check the Insurer’s Reputation: Research the insurance company’s financial stability and customer reviews.

Step 5 – Read the Fine Print: Always read the policy terms carefully, including exclusions and conditions.

Common Life Insurance Myths Debunked

Myth 1: “I’m young and healthy, I don’t need life insurance.”

Fact: The younger and healthier you are, the cheaper your premiums will be. Buying early locks in low rates.

Myth 2: “Life insurance is too expensive.”

Fact: A basic term life insurance policy can cost less than a daily cup of coffee. Affordability should not be a barrier.

Myth 3: “My employer’s life insurance is enough.”

Fact: Employer-provided group life insurance typically offers minimal coverage. It also disappears when you change jobs.

Myth 4: “Only the breadwinner needs life insurance.”

Fact: Stay-at-home parents contribute enormous financial value through childcare and household management. Their loss would create significant expenses.

Tips for Getting the Best Life Insurance Rates

- Buy when you are young and in good health

- Avoid smoking and maintain a healthy weight

- Compare at least three to five different insurance providers

- Choose term insurance if you need affordable, straightforward coverage

- Review your policy annually and update your beneficiaries when needed

Conclusion

Life insurance is not just a financial product — it is a promise to protect the people you love most. Whether you are just starting your career, raising a family, or planning for retirement, life insurance provides a critical safety net. Do not wait for the unexpected to happen. Take time to evaluate your needs, compare your options, and secure the financial future of your family today.

Frequently Asked Questions (FAQs)

Q: Can I have more than one life insurance policy?

A: Yes. Many people hold multiple life insurance policies to increase their overall coverage.

Q: Is life insurance payout taxable?

A: In most cases, life insurance death benefits are not subject to income tax. However, consult a tax advisor for specifics.

Q: What happens if I miss a premium payment?

A: Most insurers offer a grace period of 30 days. After that, the policy may lapse. Contact your insurer immediately if you face payment difficulties.

Q: Can I change my beneficiary?

A: Yes. You can update your beneficiary at any time by submitting a request to your insurance company.