Introduction

Owning a car comes with great convenience and freedom — but also significant responsibility. One of the most essential responsibilities of every vehicle owner is having proper car insurance. Whether you are buying your first car or looking to switch your existing provider, understanding how car insurance works can save you money and protect you from financial disaster on the road. This comprehensive guide covers everything from basic coverage types to tips for getting the best possible rates.

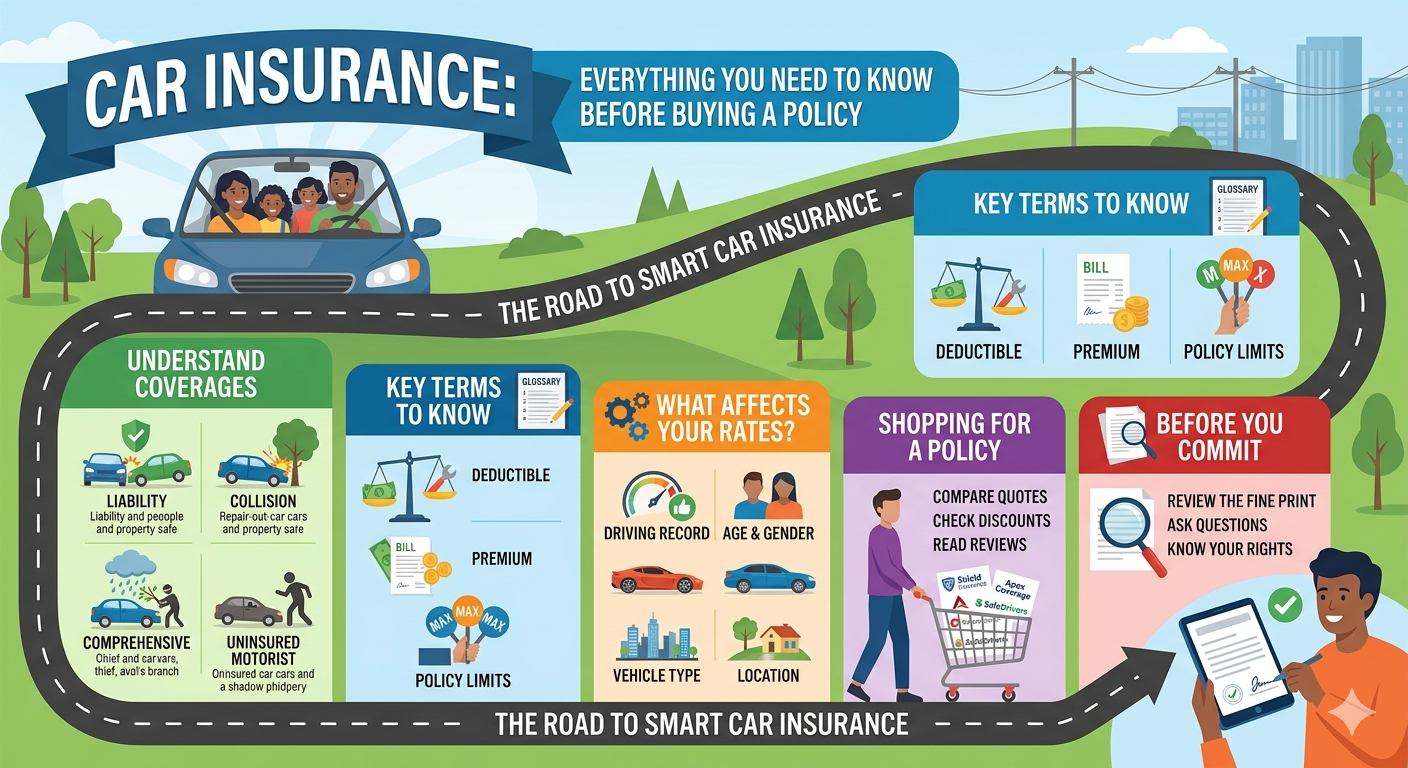

What Is Car Insurance?

Car insurance, also known as auto insurance, is a policy you purchase from an insurance company that provides financial protection against physical damage, bodily injury, and liability resulting from traffic accidents and other vehicle-related incidents. In exchange for a premium, your insurance company agrees to cover certain costs if your vehicle is involved in an accident, stolen, or damaged.

In most countries and states, having at least a minimum level of car insurance is a legal requirement. Driving without insurance can result in heavy fines, license suspension, or even imprisonment.

Why Is Car Insurance Important?

Car insurance protects you in multiple ways:

Financial Protection: Accidents can result in costly repairs, medical bills, and legal expenses. Insurance absorbs these costs so you are not financially ruined by a single incident.

Legal Compliance: Most jurisdictions require vehicle owners to carry minimum liability coverage. Insurance keeps you on the right side of the law.

Protection Against Uninsured Drivers: Not all drivers on the road are insured. Specific coverage options protect you if you are hit by an uninsured or underinsured driver.

Peace of Mind: Knowing you are covered allows you to drive with confidence, without constant worry about potential accidents.

Types of Car Insurance Coverage

Liability Insurance

Liability coverage is the foundation of most auto insurance policies and is legally required in most places. It covers two types of damages:

- Bodily Injury Liability: Pays for injuries to others caused by you in an accident.

- Property Damage Liability: Pays for damage you cause to someone else’s property, such as their vehicle or a fence.

Liability insurance does not cover your own injuries or vehicle damage.

Collision Coverage

Collision coverage pays for damage to your own vehicle resulting from a collision with another vehicle or object, regardless of who is at fault. This coverage is particularly valuable for newer or more expensive vehicles.

Comprehensive Coverage

Comprehensive coverage protects your vehicle against non-collision damage, including theft, vandalism, natural disasters, fire, falling objects, and animal collisions. If you live in an area prone to extreme weather or high car theft, comprehensive coverage is highly recommended.

Personal Injury Protection (PIP)

Also known as “no-fault insurance,” PIP covers medical expenses for you and your passengers regardless of who caused the accident. Some policies also cover lost wages and rehabilitation costs.

Uninsured/Underinsured Motorist Coverage

This coverage protects you if you are involved in an accident caused by a driver who has no insurance or insufficient insurance to cover the damages. Given the number of uninsured drivers on the road, this is a wise investment.

Gap Insurance

If you have a car loan or lease, gap insurance covers the difference between what your car is worth (actual cash value) and what you still owe on the loan. This is critical if your car is totaled and the payout does not cover your remaining loan balance.

Factors That Affect Your Car Insurance Premium

Insurance companies calculate your premium based on several risk factors:

- Driving Record: Drivers with clean records pay significantly less. Accidents, speeding tickets, and DUI convictions raise your premium considerably.

- Age and Experience: Young and inexperienced drivers are considered higher risk and pay higher premiums. Rates typically drop after age 25.

- Vehicle Type: The make, model, age, and safety features of your car influence your premium. Luxury cars and sports cars cost more to insure.

- Location: Living in an urban area with heavy traffic, high crime rates, or extreme weather increases your risk profile and premium.

- Annual Mileage: The more you drive, the greater your exposure to accidents. High-mileage drivers pay more.

- Credit Score: In many countries, insurers use your credit score as a risk indicator. A higher credit score can lead to lower premiums.

- Coverage Amount and Deductible: Higher coverage limits raise your premium, while a higher deductible reduces it.

How to Save Money on Car Insurance

Getting affordable car insurance does not mean cutting corners on coverage. Here are proven strategies to lower your premiums:

Compare Multiple Quotes: Shop around and get quotes from at least three to five different insurers. Prices can vary dramatically for the same coverage.

Bundle Your Policies: Many insurers offer discounts if you purchase multiple policies, such as home and auto insurance, from the same company.

Maintain a Clean Driving Record: Avoid traffic violations and accidents to keep your risk profile low.

Increase Your Deductible: Choosing a higher deductible reduces your monthly premium. Just ensure you can afford the deductible if you need to file a claim.

Take a Defensive Driving Course: Many insurers offer discounts for completing an approved defensive driving course.

Install Safety Features: Anti-theft devices, dashcams, and advanced safety systems can qualify you for discounts.

Ask About Discounts: Inquire about good student discounts, low-mileage discounts, loyalty discounts, and professional association discounts.

What to Do After a Car Accident

If you are involved in a car accident, follow these steps to protect yourself and facilitate the insurance claims process:

- Ensure Safety First: Check for injuries and call emergency services if needed.

- Move to Safety: Move vehicles out of traffic if possible.

- Call the Police: A police report is often required for insurance claims.

- Exchange Information: Collect the other driver’s name, contact info, license plate number, and insurance details.

- Document the Scene: Take photographs of the vehicles, damage, and surrounding area.

- Notify Your Insurer: Contact your insurance company as soon as possible to report the accident.

- Seek Medical Attention: Even if you feel fine, get a medical evaluation — some injuries appear days later.

Conclusion

Car insurance is a non-negotiable part of responsible vehicle ownership. It protects your finances, your passengers, and other road users in the event of an accident. Understanding the different coverage types, the factors that influence your premium, and how to save money empowers you to make smart insurance decisions. Always review your policy annually and update your coverage as your life circumstances change. Drive safely — and drive insured.

Frequently Asked Questions (FAQs)

Q: Is car insurance mandatory everywhere?

A: In most countries, at least liability insurance is legally required to operate a vehicle on public roads.

Q: Does car insurance cover a rental car?

A: Many comprehensive policies extend coverage to rental cars. Check your policy or call your insurer before renting.

Q: Will my premium increase after filing a claim?

A: Filing a claim, especially for an at-fault accident, can raise your premium at renewal. Consider whether the claim is worth filing for minor damages.

Q: How do I switch car insurance providers?

A: You can switch at any time. Purchase your new policy first, then cancel your old one to avoid any gap in coverage.