Introduction

Healthcare costs are rising every year across the globe. A single hospital visit, surgery, or long-term illness can create a financial burden that devastates families without adequate preparation. Health insurance exists to shield individuals and families from these unexpected medical expenses. In this detailed guide, we will walk you through everything you need to know about health insurance — from the basics to choosing the right plan for your unique situation.

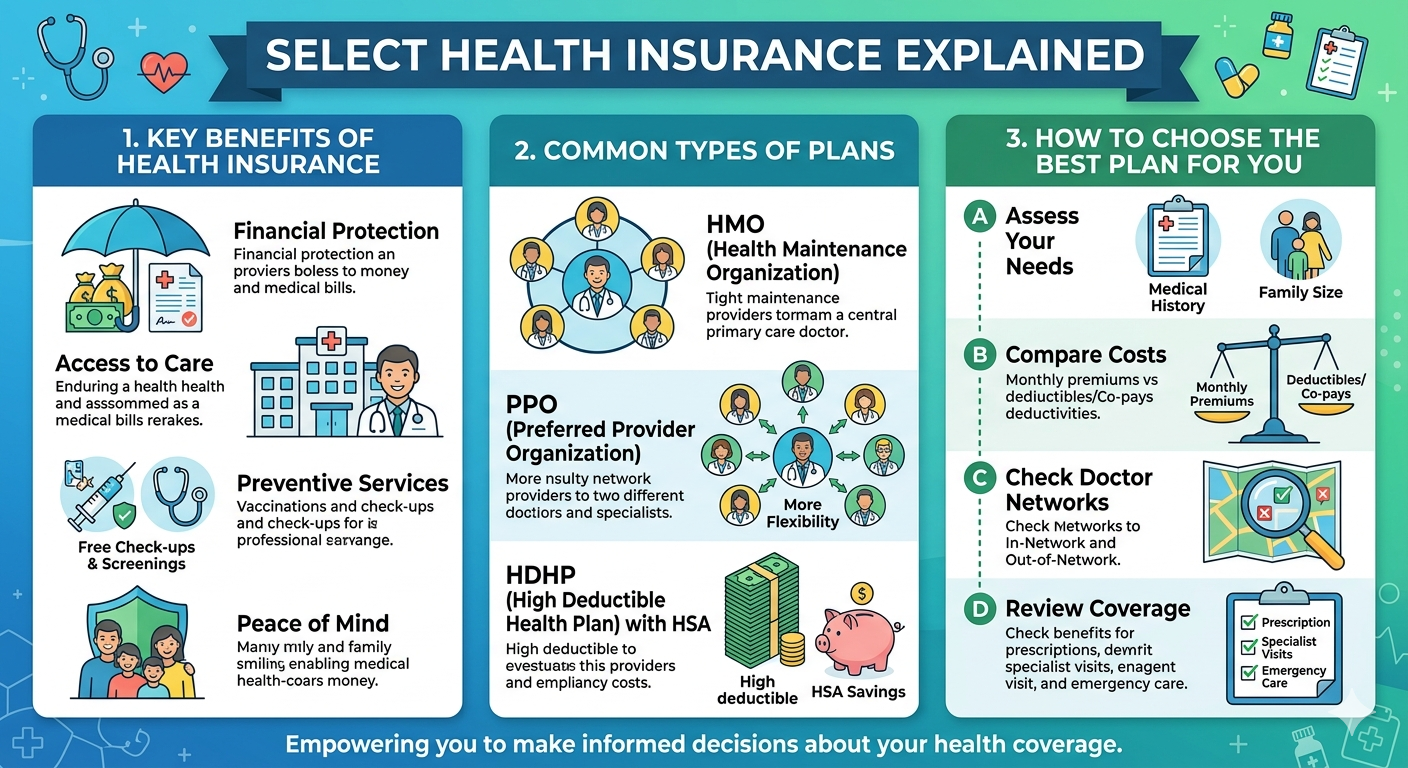

What Is Health Insurance?

Health insurance is a type of coverage that pays for medical and surgical expenses incurred by the insured individual. In exchange for a monthly premium, the insurance provider agrees to cover all or a portion of the costs associated with doctor visits, hospital stays, prescription medications, preventive care, and other health-related services.

Health insurance can be provided by an employer, purchased independently, or obtained through government programs. Regardless of the source, its fundamental purpose remains the same: to reduce the financial risk associated with illness and injury.

Key Terms You Need to Know

Before diving deeper, it helps to understand some common health insurance terminology:

Premium: The monthly amount you pay to maintain your health insurance coverage, regardless of whether you use medical services.

Deductible: The amount you must pay out of pocket before your insurance begins covering costs. For example, if your deductible is $1,000, you pay the first $1,000 of covered medical expenses each year.

Copayment (Copay): A fixed amount you pay for a specific medical service, such as $20 for a doctor’s visit.

Coinsurance: The percentage of costs you share with your insurer after meeting your deductible. For example, if your coinsurance is 20%, you pay 20% and your insurer pays 80%.

Out-of-Pocket Maximum: The most you will have to pay for covered services in a year. After reaching this limit, your insurance covers 100% of additional costs.

Network: The group of doctors, hospitals, and healthcare providers that have agreements with your insurance company to provide services at reduced rates.

Types of Health Insurance Plans

Health Maintenance Organization (HMO)

HMO plans require you to choose a primary care physician (PCP) who coordinates all your healthcare. Referrals from your PCP are required to see specialists. These plans typically have lower premiums but limited provider networks.

Preferred Provider Organization (PPO)

PPO plans offer more flexibility. You can visit any doctor or specialist without a referral, both inside and outside your network. However, staying within the network results in lower costs. PPOs usually have higher premiums than HMOs.

Exclusive Provider Organization (EPO)

EPO plans only cover services provided by doctors and hospitals within the plan’s network. Unlike HMOs, you do not need a referral to see a specialist. These plans offer moderate premiums and are a middle ground between HMO and PPO plans.

Point of Service (POS)

POS plans combine features of HMO and PPO plans. You choose a PCP within the network but can seek care outside the network at a higher cost. Referrals are required for specialist visits.

High-Deductible Health Plans (HDHP)

HDHPs have lower monthly premiums but higher deductibles. They are often paired with a Health Savings Account (HSA), which allows you to save pre-tax money for medical expenses.

Benefits of Having Health Insurance

- Financial Protection: Health insurance prevents a medical emergency from wiping out your savings or plunging your family into debt.

- Access to Preventive Care: Many health insurance plans cover preventive services such as annual checkups, vaccinations, and cancer screenings at no additional cost.

- Better Health Outcomes: Insured individuals are more likely to seek medical care early, leading to earlier diagnoses and better health outcomes.

- Mental Health Coverage: Modern health insurance plans often include mental health services, therapy, and substance abuse treatment.

- Prescription Drug Coverage: Insurance plans help reduce the often-steep costs of prescription medications.

- Maternity and Newborn Care: Comprehensive health plans cover prenatal care, childbirth, and newborn care services.

How to Choose the Right Health Insurance Plan

Choosing the right plan depends on several factors unique to your personal situation:

Step 1 – Evaluate Your Health Needs: Consider your medical history, frequency of doctor visits, and any ongoing prescriptions.

Step 2 – Calculate Total Costs: Do not focus only on premiums. Factor in deductibles, copays, and coinsurance to understand your true annual cost.

Step 3 – Check the Provider Network: Make sure your preferred doctors and hospitals are included in the plan’s network.

Step 4 – Review the Drug Formulary: If you take regular medications, check whether they are covered and at what cost.

Step 5 – Consider Your Family’s Needs: If covering a spouse and children, look for family-friendly plans with comprehensive pediatric coverage.

Step 6 – Compare Multiple Plans: Use online comparison tools or work with a licensed insurance broker to evaluate multiple options side by side.

Common Health Insurance Mistakes to Avoid

Choosing the cheapest plan without checking coverage: A low-premium plan with high deductibles may cost you more in the long run.

Not updating your plan annually: Your health needs change. Review your plan every year during open enrollment.

Ignoring the network: Using out-of-network providers can result in significantly higher costs or denied claims.

Skipping preventive care: Many insured individuals do not use their free preventive services, missing early detection opportunities.

Not understanding your policy: Always read your policy document carefully to know what is and is not covered.

Health Insurance for Self-Employed Individuals

If you are self-employed or a freelancer, obtaining health insurance independently is crucial. Options include:

- Health insurance marketplaces or government exchanges

- Short-term health insurance plans

- Joining a professional association that offers group health coverage

- Health-sharing ministries (as an alternative, though not traditional insurance)

Many self-employed individuals qualify for premium tax credits based on income, which can significantly reduce the cost of coverage.

Conclusion

Health insurance is not a luxury — it is a necessity in today’s world. Medical emergencies are unpredictable, and the financial consequences of being uninsured can be devastating. By understanding the different types of health insurance, key terminology, and how to evaluate your options, you can make an informed decision that protects both your health and your financial well-being. Investing in health insurance today means investing in a safer, healthier tomorrow.

Frequently Asked Questions (FAQs)

Q: What is the best health insurance plan for a family?

A: It depends on your family’s health needs and budget. PPO plans offer the most flexibility, while HMO plans provide cost savings.

Q: Can I get health insurance if I have a pre-existing condition?

A: In many countries, insurers are prohibited from denying coverage or charging more based on pre-existing conditions. Check local regulations for specifics.

Q: Is dental and vision coverage included in health insurance?

A: Standard health insurance plans do not always include dental and vision coverage. These may require separate or supplemental plans.

Q: What happens if I don’t have health insurance?

A: Without insurance, you are responsible for 100% of all medical costs. In some regions, going uninsured may also result in financial penalties.